It has been a tough year for diversified futures traders. Most big name funds lost money last year and the whole industry suffered from the binary risk on/risk off scenario we have been seeing during much of last year. Our core DFT strategy had a less than stellar run but it kept up with competition and it never saw any drawdowns near what the buy and hold equity crowed suffered through. Compared to our futures competitors, we experienced a higher volatility during the second part of the year than most of them, where we first had large gains and then had to give most of it up in the currency/commodity reversal of early October. These years are part of the game and the cost of doing business in the futures markets. They will come around now and then and they will always be painful, but the good years will pay for them and more.

The performance against the world equity markets is a mixed blessing. In the past 12 months, the return from the equities would have been slightly higher although you would have lost money on both alternatives. The equity index saw much greater drawdowns but it is now recovering and just took the lead over the futures. Over longer time periods, the equity markets have never managed to keep up with diversified futures. How long will it last this time?

In the past year we have seen very consistent portfolios where the trends have been reflecting either a risk on or a risk off scenario and there has been a worrying degree of correlation between the positions. Such situations are inherently negative for diversified futures trading, as there is little diversification to be had, and they generally occur when the markets are driven by a single or a small number of related macro developments. In the past year this factor was of course the fate of the Eurozone. The current portfolio looks much more interesting as it contains more and more bets which in a risk on/risk off scenario should be contradictory.

We still hold a large amount of risk on the long rates bet as well as the long dollar. These are traditionally risk off bets. The risk on side is increasing however, with positions in long equtiies and long energies added recently and we are now approaching a real diversified portfolio.

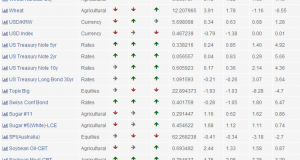

Current holdings:

| Market | Direction | Sector | Entry Date |

|---|---|---|---|

| Coffee | Short | Agricultural Commodities | 2011-12-13 |

| Sugar #11 | Short | Agricultural Commodities | 2011-11-25 |

| Rice-Rough | Short | Agricultural Commodities | 2011-11-10 |

| Oats | Short | Agricultural Commodities | 2012-01-13 |

| Hogs-Lean(Floor Trading Only) | Short | Agricultural Commodities | 2012-01-12 |

| Swedish Krona/U.S. Dollar | Short | Currencies | 2011-11-28 |

| Swiss Franc | Short | Currencies | 2011-11-28 |

| Norwegian Krone/U.S. Dollar | Short | Currencies | 2011-12-15 |

| Euro | Short | Currencies | 2011-12-13 |

| Australian Dollar | Long | Currencies | 2012-01-18 |

| British Pound | Short | Currencies | 2011-12-30 |

| Nasdaq 100 | Long | Equities | 2012-01-19 |

| S&P 500 | Long | Equities | 2012-01-11 |

| FTSE 100 Index | Long | Equities | 2012-01-11 |

| Gasoline | Long | Non-Agricultural Commodities | 2012-01-19 |

| Silver-COMEX | Short | Non-Agricultural Commodities | 2011-12-15 |

| Crude Oil-Light | Long | Non-Agricultural Commodities | 2012-01-04 |

| Natural Gas-Henry Hub | Short | Non-Agricultural Commodities | 2011-07-08 |

| Japanese 10yr Govt Bond | Long | Rates | 2012-01-12 |

| T-Note-U.S. 2 Yr | Long | Rates | 2011-12-08 |

| T-Note-U.S. 10 Yr w/Prj AX | Long | Rates | 2011-12-14 |

| Australian Govt Bond 6%(10Yr) | Long | Rates | 2011-11-21 |

| T-Bond-U.S. | Long | Rates | 2011-12-19 |

| T-Note-U.S. 5 Yr | Long | Rates | 2011-12-08 |

| Gilt-Long(8.75-13yr) | Long | Rates | 2011-11-16 |

| Canadian Bankers' Acceptance-3Mth-ME (24 hr) | Short | Rates | 2012-01-03 |

| Canadian Govt Bond 10Yr | Long | Rates | 2011-11-24 |

| Euro German Bund | Long | Rates | 2012-01-10 |

| Euro German Bobl | Long | Rates | 2011-12-15 |

| Euro German Schatz | Long | Rates | 2011-11-10 |