The current trend following portfolio has a very clear tilt towards the long side of, well, just about everything. We are long rates, long equities, long metals, long energies and even a little bit of long agriculturals. To be fair, we also have a few short positions but they are rather the exception at the moment. There is also quite a high number of positions open and given that each position is sized to have a theoretical equal risk, this means quite a high portfolio risk open.

You may wonder why it matters if our positions are long or short, given that the strategy is symmetrical and that there is a clear negative correlation between some of these positions. In the currency sector you could also argue that the distinction between long and short is rather arbitrary, as you are always long one currency and short the other. But, it still does matter if we have long or short positions.

Long positions are generally more profitable than the short positions and this has a very simple explanation. In part there is the asymmetrical volatility profile that many asset classes show where they tend to have choppier and more violent moves in a bear market than a bull market, but this is not the main story. The bigger story is much simpler. Our aim is to hold good positions for as long as possible and the really great positions which pay for a lot of the smaller losses will end up making quite substantial moves. If you have a long position which goes in your favor, it will grow larger with success and you will achieve a compound effect on your profits. On the other hand, if your short position goes in your direction, it will shrink to a smaller position the more profitable it becomes. The profit potential of a short position is lower than that of a long position.

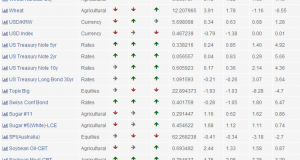

| Market | Direction | Sector | Entry Date |

|---|---|---|---|

| Cattle-Live | Long | Agricultural Commodities | 2012-01-25 |

| Coffee | Short | Agricultural Commodities | 2011-12-13 |

| Oats | Short | Agricultural Commodities | 2012-01-13 |

| Orange Juice-Frozen | Long | Agricultural Commodities | 2012-01-23 |

| Sugar #11 | Short | Agricultural Commodities | 2011-11-25 |

| Rice-Rough | Short | Agricultural Commodities | 2011-11-10 |

| New Zealand Dollar | Long | Currencies | 2012-01-26 |

| Australian Dollar | Long | Currencies | 2012-01-18 |

| Japanese Yen | Long | Currencies | 2012-01-31 |

| S&P 500 | Long | Equities | 2012-01-11 |

| Nasdaq 100 Index | Long | Equities | 2012-01-19 |

| Dax Index | Long | Equities | 2012-01-27 |

| DJ Euro STOXX 50 Index | Long | Equities | 2012-02-02 |

| CAC 40 Index | Long | Equities | 2012-02-02 |

| FTSE 100 Index | Long | Equities | 2012-01-11 |

| Crude Oil-Light | Long | Non-Agricultural Commodities | 2012-01-04 |

| Gasoline-Reformulated Blendstock | Long | Non-Agricultural Commodities | 2012-01-19 |

| Gold | Long | Non-Agricultural Commodities | 2012-02-03 |

| Canadian Bankers' Acceptance-3Mth-ME (24 hr) | Short | Rates | 2012-01-03 |

| Short Sterling | Long | Rates | 2012-02-03 |

| Canadian Govt Bond 10Yr | Long | Rates | 2011-11-24 |

| T-Bond-U.S. | Long | Rates | 2011-12-19 |

| T-Note-U.S. 10 Yr w/Prj AX | Long | Rates | 2011-12-14 |

| T-Note-U.S. 2 Yr | Long | Rates | 2011-12-08 |

| Euro German Bobl | Long | Rates | 2011-12-15 |

| Gilt-Long(8.75-13yr) | Long | Rates | 2011-11-16 |

| Euro Swiss Franc | Short | Rates | 2012-01-23 |

| EURIBOR-3 Mth | Long | Rates | 2012-01-23 |

| T-Note-U.S. 5 Yr | Long | Rates | 2011-12-08 |

| Japanese 10yr Govt Bond | Long | Rates | 2012-01-12 |

| Euro German Schatz | Long | Rates | 2011-11-10 |

| Eurodollar-3 Mth | Long | Rates | 2012-01-26 |

| Euro German Bund | Long | Rates | 2012-01-10 |

The world equity markets has had a good run lately but unfortunately the trend followers have failed to keep up. Don’t worry, this is not an unusual situation and the futures will catch up again as they always have done in the past. The year to date return as of yesterday was -2.8%.