Decouple. The most overused word in financial analysis letters. An in hard competition at that. We are not looking at a full decouple for sure, but what we see lately is a little bit less correlation between asset classes and possibly the beginning of the end or at least at respite in the whole ‘risk on/risk off’ regime. For the pat 6-9 months, the markets have very much been in this type of regime, where everything has a very high correlation regardless of fundamental sanity and each asset and instrument need to chose a side. A line has been drawn in the sand where risk on is on one side and risk off on the other. The distinction between the two sometimes makes little sense but arguing with the market mechanics is often akin to arguing with a locked door.

What we see lately is a slight decrease in the extreme correlations from the past year and some markets start moving by their own force. The dollar is a good example as it has been a risk on trade for some time and it still holds some sensitivity to the negative moves in the market, but it has managed to retain a strong positive trend despite the strong equities lately. We even have such a counter intuitive phenomenon going on as strong equities and strong bonds.

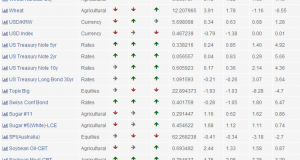

The core trends at the moment are, in order of importance, long rates, long dollar and short commodities. As an emerging bet which will likely grow in size if the inertia continues is the long equities. In the recent past, long dollar should be counter to long equities, but in line with long rates and short commodities. The fact that we see these shifting allegiances is encouraging since strong intramarket correlations is certainly a negative influence on diversified futures strategies. When correlations increase, the benefits of diversification decreases and what seems like a nice balanced portfolio turns out to be just a single huge bet with very big risks. What we want to see is as low intramarket correlations as possible.

Current holdings:

| Market | Direction | Sector | Entry Date |

|---|---|---|---|

| Rice-Rough | Short | Agricultural Commodities | 2011-11-10 |

| Sugar #11 | Short | Agricultural Commodities | 2011-11-25 |

| Oats | Short | Agricultural Commodities | 2012-01-13 |

| Coffee | Short | Agricultural Commodities | 2011-12-13 |

| Hogs-Lean(Floor Trading Only) | Short | Agricultural Commodities | 2012-01-12 |

| Swedish Krona/U.S. Dollar | Short | Currencies | 2011-11-28 |

| Swiss Franc | Short | Currencies | 2011-11-28 |

| British Pound | Short | Currencies | 2011-12-30 |

| Euro | Short | Currencies | 2011-12-13 |

| Norwegian Krone/U.S. Dollar | Short | Currencies | 2011-12-15 |

| S&P 500 | Long | Equities | 2012-01-11 |

| FTSE 100 Index | Long | Equities | 2012-01-11 |

| Natural Gas-Henry Hub | Short | Non-Agricultural Commodities | 2011-07-08 |

| Crude Oil-Light | Long | Non-Agricultural Commodities | 2012-01-04 |

| Silver-COMEX | Short | Non-Agricultural Commodities | 2011-12-15 |

| Gold-COMEX | Short | Non-Agricultural Commodities | 2011-12-30 |

| T-Note-U.S. 2 Yr | Long | Rates | 2011-12-08 |

| T-Note-U.S. 10 Yr w/Prj AX | Long | Rates | 2011-12-14 |

| Australian Govt Bond 6%(10Yr) | Long | Rates | 2011-11-21 |

| Euro German Bobl | Long | Rates | 2011-12-15 |

| Australian Govt Bond 6%(3Yr) | Long | Rates | 2011-11-11 |

| T-Bond-U.S. | Long | Rates | 2011-12-19 |

| Euro German Schatz | Long | Rates | 2011-11-10 |

| Canadian Bankers' Acceptance-3Mth-ME (24 hr) | Short | Rates | 2012-01-03 |

| Gilt-Long(8.75-13yr) | Long | Rates | 2011-11-16 |

| Euro German Bund | Long | Rates | 2012-01-10 |

| Canadian Govt Bond 10Yr | Long | Rates | 2011-11-24 |

| T-Note-U.S. 5 Yr | Long | Rates | 2011-12-08 |

| Japanese 10yr Govt Bond | Long | Rates | 2012-01-12 |

Current allocation:

Performance Update: